Analyzing the financial condition of companies

ass: Fattoyev Elbek Alisherovich

elbekjonfea@gmail.com

Tashkent University of Applied Sciences

Department of General Economics

https://doi.org/10.5281/zenodo.10467829

Abstract

In our article, information is provided about the methods of analyzing the financial condition of companies and its

importance. Information is also given about the possible outcomes of this analysis for financial management and

administration. The implementation of financial analysis based on accounting reports, the utilization of this

analysis for various purposes, and the evaluation of information are discussed.

Key words

High-level condition, Internal analysis, Financial managers, Financial analysis, Financial management, asset

management, Budget report, market economy, External analysis, External economic environment, classification,

Debtor, report, growth, currency movement, analysis, Accounting balance.

1 INTRODUCTION

The financial condition of enterprises is an

economic indicator, and its importance is very

significant, especially in the conditions of market

economy, knowing the theoretical foundations of

enterprises' independent activities at a time when

their activities are growing gains special importance.

The financial situation of companies is

changing very quickly. This in turn increases the

importance of analyzing the financial situation of

companies.

The financial condition of enterprises can

be assessed by expressing the method of evaluating

in traditional terms, and this also enables forecasting

the financial condition of enterprises according to

the accounting report. This financial analysis is

carried out.

Financial analysis is usually divided into

two types - internal and external. Internal analysis is

carried out by financial managers of companies.

External analysis, on the other hand, is conducted by

individuals who come from outside, such as auditors.

The analysis of the financial situation of

companies serves several purposes, including:[1]

Determine the financial situation;

Determining the change in financial

condition at a certain time;

Identifying the main factors causing

changes in the economic situation;

Analyze the economic situation using

economic-mathematical methods and modern

computer programs;

The purpose of financial analysis, along

with cooperation, should not only be limited to

determining the financial condition of companies,

but also to constantly improve their financial

situation as much as possible.

Financial analysis helps to identify

weaknesses and provide opportunities to eliminate

those weaknesses. Therefore, financial analysis is a

management tool in modern conditions.

Financial analysis is considered the main

role

of

financial

management.

Financial

management is the art of managing the financial

conditions of companies. This management art is

used in the effective utilization of financial

strategies. It plays its role in internal and external

diagnosis.

The identification of internal factors is used

to improve the management of assets, i.e. it is used

in the use of valuable papers.

- Study the price dynamics of goods.

-tax office (tax collection agency) and bank

credit deposits, securities issuance:

- Activities of competitors in the financial

and commodity markets and the like:

Financial analysis conducted provides

alternative solutions and the possibility of

monitoring them.

Internal users (employees and managers)

assess their financial performance and identify its

growth trends based on the accounting report. The

accounting report is the main database that

determines the company's investment and financial

status.

It is possible to make the following decisions with

the help of financial analysis:

1. Short-term financial management of companies

(filling out balance sheets).

2. Long-term financial

management (capital investment, profitable

investment securities, and issuance of valuable

papers).

Paying dividends to shareholders.

3. Mobilizing economic growth opportunities

(increasing sales and profit growth).

4. Financial analysis shows the correlation between

the implementation of accounting information and

the financial solution accepted by company leaders.

1.1. Heading. The source of information for

financial analysis based on accounting reports.

Providing users with complete and accurate

information about the financial condition of

companies is the fundamental basis of international

standards on the issue of financial reporting, and it

establishes the concept of modern financial

reporting development.

Therefore, users can evaluate the company's

capabilities, shape their profits, and accept the

established management solution by constantly

analyzing information at any given time.

Now let's consider the interdependence of financial

and management analysis.

Financial analysis is a component of companies'

economic activity and is closely related to the

following sections:

1. Financial analysis;

2. Production management analysis;

The classification of financial analysis is closely

related to accounting

(financial) and management accounting in practice.

This classification is conditional, and it is possible

to interpret internal analysis and external analysis.

1.2.

Relationship

between

financial

and

management analyses.

The degree and content of financial analysis are

largely dependent on the completeness and accuracy

of the information obtained, as well as various other

factors.

Annual reports allow for a thorough analysis of a

company's financial condition beyond its financial

performance.

Until January 1, 1997, the following reports

formed the basis for financial analysis:

1. Report No. 1 - by form (consistency of

companies).

2. Report No. 2 - by form (financial results report).

3. Report No. 1-f - by form (report on main

financial indicators of companies).

4. Report No. 2-f - by form (report on composition

of company expenses).

5. Report No. 5 - by form (addition to the

consistency of companies).

In addition, the use of the following indicators is

relevant for analyzing the financial condition of a

company:

- investment activity

- movement of debt amounts

- debtor-creditor debts

- composition of non-current assets at the end of

the year

- status and movement of main investments

- financial ratios

- currency movements

The above information allows for a comprehensive

analysis of the financial condition of bank

companies.

Based on the Regulation on Approval of Forms and

Volume of Quarterly and Annual Financial Reports

of Companies adopted by the Ministry of Finance of

the Republic of Uzbekistan on January 15, 1997, the

following financial reports have been approved:

1. Annual financial report for the analysis of the

financial condition of companies.

No. 1 - Form "Balance Sheet"

No. 2 - Form "Financial Statement"

No. 2 - A - Form "Information on Debts and

Credits"

No. 3 - Form "Report on Movement of

Main Amounts"

No. 4 - Form "Report on Cash Flow"

2. Semi-annual financial report for the

analysis of the financial condition of companies.

No. 1 - Form "Balance Sheet"

No. 2 - Form "Financial Statement"

No. 2 - A - Form "Information on Debts and

Credits"

No. 3 - Form "Report on Cash Flow"

3. Quarterly financial report for the analysis of the

financial condition of companies.

No. 1 - Form "Balance Sheet"

No. 2 - Form "Financial Statement"

No. 2 - A - Form "Information on Debts and

Credits"

In the newly approved form of the financial report,

not only has it changed, but its content has been

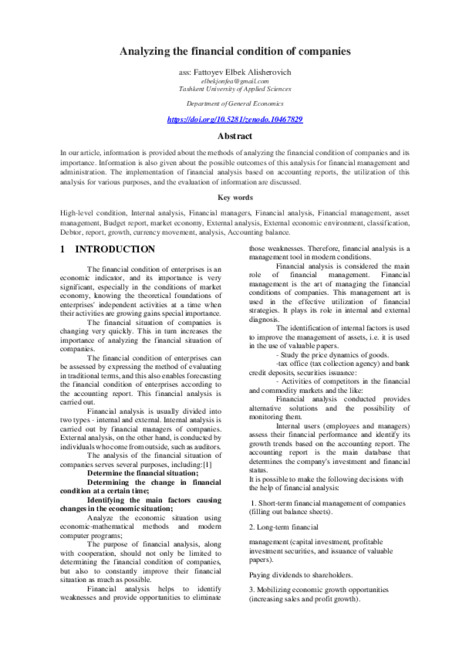

Analysis of

economic

activity

Financial analysis

based on the

bugalteria report

Domestic financial

stable based on the

buggalteria report

Analysis of the

internal production of

the farm on the basis

of management

Financial

analysis

Management

analysis

Analysis of

economic

activity

Financial analysis

Accounting report

Internal financial

analysis based on

accounting report

Management

analysis

Analysis of the

internal production

of the farm on the

basis of management

significantly improved, meaning that the

information has been structured. Now the balance

sheet consists of two sections, not three.

The information on debts and credits includes both

national and foreign information.

Now let's look at the methods of financial analysis.

The purpose of financial analysis is to determine

the financial condition of companies using specific

quantitative indicators. These indicators include:

- Changes in the structure of assets and liabilities.

- Dynamics of changes in debt and credit positions.

The level of profitability of assets (

liabilities).

In practice, the following methods of financial

analysis can be indicated:

- Horizontal analysis

- Vertical analysis

- Trend analysis

- Comparative analysis

- Ratio analysis

1) Horizontal analysis based on timely analysis

compares the indicators of financial reporting with

previous period indicators. The main methods of

horizontal analysis are as follows:

- Simple comparison of reports and analysis of their

sharp differences;

- Analysis of financial indicators with their trend.

In this case, the main attention is paid to the fact

that the change of one indicator does not

correspond to the change of the second indicator.

2) Vertical analysis is used to compare certain

sections of the balance sheet and is used to compare

the final indicator with the results in the next

period.

3) Trend analysis is mainly used to determine the

relative decline from the base period for the

analysis of financial indicators (for quarterly,

annual periods).

4) Comparative analysis means comparing certain

indicators of enterprises within the industry, as well

as comparing industry indicators.

5) Ratio analysis examines the impact of certain

factors (ratios) on the performance indicator. This

method uses correlation analysis.

As an example of ratio analysis, we can mention

DuPont's three-factor model:

'V.V. Bocharov. Financial Analysis

ck

SF

SF

AF

A

SF

X

X

CK

AF

A

CK

=

=

SF - net profit here

is the net profitability of equity. (in percentage or

in one unit)

CK - capital at the end of the reporting period.

AF - profit obtained from the allocation of the

product

A - assets at the end of the reporting period

According to the analysis of the accounting report,

if the net profit [3]

(derived from equity) is lower, then the factor that

caused the decrease is determined. These factors are

as follows:

1. Decrease in net profit;

2. Inefficient management of assets;

3. Changes in the composition of invested capital;

Example. According to the first stage of the report,

net profit is 9 million som, income from allocation

is 60 million som, assets are 120 million som,

equity is 30 million som. According to the second

stage of the report, net profit is 9.9 million som,

income from allocation is 63.6 million som, assets

are 126 million som, equity is 30 million som.

9

60

120

100 30 30%

60

120

30

CKI

SF

X

X

X

=

= =

9.9

63.6

126.0

100 33%

63.6

126.0

30.0

CKII

SF

X

X

X

=

=

1)

Here, as a result of the increase in net profit,

the increase in the return on equity was equal

to 1.14% (31.14-30.0).

9.9

60

120

100 31.14%

63.6

120

30

X

X

X

=

2)

As a result of accelerating asset turnover, the

increase in the return on equity was equal to

0.3% (30.3 - 30.0).

9

63.6

120

100 30.3%

120

126.0

30

X

X

X

=

3)

Taking into account the change in the

capital structure, the increase in the return

on equity was equal to 1.5% (31.5 - 30.0).

9

60

126

100 31.5%

120

120

30

X

X

X

=

4) If we add these three factors together:

1.14 + 0.3 + 1.5 = 2.94%

Or approximately 3%.

The financial coefficient method is used to

determine

the

interdependence

of

financial

indicators.

In the analysis, the following factors need

to be taken into account: the efficiency of the applied

accounting methods, the accuracy of financial

reporting, various calculation methods, and the

compatibility of the used coefficients with statistical

data.

These three coefficients are widely used in

the practice of developed Western corporations

(USA, Canada, Great Britain):

ROA, ROE, ROC

Income from total assets.

(

)

net income

1-tax rate percentage

total assets

X 100

ROA

+

=

Investment capital, or more specifically

long-term capital, represents a long-term contractual

agreement. Therefore, it represents long-term

financial resources:

Income from investment capital

(

)

(

)

net profit

tax rate long in percentage

term contract

faithful capital

1

C

RO

+

−

=

+

It is known that the identification system, which is

necessary for assessing the economic difficulties

and ensuring their survival, is an indicator system

that is used to identify the ratio of continuous

changes or concepts, one of which is the corporate

balance sheet.

The balance sheet is a continuous changing event or

concept indicator system that represents the ratio of

the national economy's development in accordance

with its goals and ensures its efficiency. National

economic sectors, such as monetary, intersectoral

payments, value, labor resources, fuel, energy,

profit balances, population income and expenditure

balances, and accounting balances, have such

balances.

The balance sheet method is when everything that

needs to be taken into

account is taken into account on both sides, that is,

it shows what and how much money has been spent

on the item being accounted for. The balance sheet

is always presented as a table consisting of two

parts. The active (left side) part of the balance sheet

includes assets, while the passive (right side) part

indicates their acquisition or formation sources. The

ratio between assets and liabilities must always be

equal.

It is well known that the balance sheet plays

a key role in assessing the financial situation of

companies. Taking this into account, let's take a

detailed look at the composition of the balance sheet.

From the perspective of ownership form, the

following report forms were recommended by Order

No. 5 of the Ministry of Finance of the Republic of

Uzbekistan dated January 15, 1997 for quarterly

reporting to entities engaged in economic

activities:[2]

Composition of the Accounting Balance Sheet.

The symbols used in economic analysis and their

meanings

UM.yb - Own funds at the beginning of the year

UM.yo - Own funds at the end of the year

B - Total assets (liabilities) or balance sum

AV - Main assets

MX - Debts for labor remuneration

UMA - Long-term assets

Am - Current liabilities

UMM - Long-term liabilities

ChJM.yb - Borrowed funds at the beginning of the

year

ChJM.yo - Borrowed funds at the end of the

year

ChJM - Borrowed funds

UMCHJM - Long-term borrowed funds

KMCHJM - Short-term borrowed funds

D - Debtors

KR - Creditors

UZAM - Share of own funds in current liabilities

(balances of own funds in current liabilities)

ChJM.am - Balances of borrowed funds in current

liabilities

PM - Cash amounts

UMA.yb - Long-term assets at the beginning of the

year

1- Title

"Balance

Sheet"

Active

long-term

assets

circulatin

g assets

passive

individua

l funds

liabilities

1-P shape. Labor report

1. Number of workers

and wages

2. Amount of urine,

under contract

working workers. the

worker

movement of forces,

vacancy

amount of seats, notolah

wealth

1- Title "Balance Sheet"

Assets

1. Long-term assets

1.1. Fixed assets (main

equipment)

1.2. Current assets

1.3. Capital investments

1.4 Long-term

investments,

subsidiaries,

and joint ventures

2. Current assets

2.1. Monetary assets

2.2 Cash amounts

2.3 Marketable

securities

2.4 Accounts receivable

All assets

Passives

1. Sources of own funds

1.2. Charter fund

1.3. Additional capital

1.4. Undistributed profit

2. Liabilities

2.2. Long-term liabilities

2.3. Short-term liabilities

2.3.1. Including short-term

loans

2.4. Creditors

Including:

2.4.1. Debts for labor

remuneration

2.4.2. Debts to the budget

All passives

UMA.yo - Long-term assets at the end of the year -

Total own funds

OA - Current assets

MAM - Monetary current liabilities

ICHZ - Production costs

TICH - Unfinished production

TM - Finished products

OST - Goods for sale

VM - Currency amounts

KPM - Cash in hand[6]

The interrelation of selected indicators for

analyzing the company's balance.

It is possible to identify many indicators necessary

for analyzing and assessing the financial balance of

the accounting through this interdependence.

For example, the sources of revolving funds:

(Mam+D+Pm+) = [(Um+ChJUM) - (AV+NA)] +

(ChJKM+KP)

In this case: the value of the revolving funds (AM) is

the value of the revolving funds;

[(UM+ChJUM) - (AV+NA)] is the accumulated

amount of revolving funds from their own funds

(Umap)

(ChJKM+KR) is the accumulated amount of

revolving funds from external sources (ChJAM).

Based on these interdependencies, it is possible to

analyze the financial balance in a general way.

Therefore, in this section, we have examined the

importance of analyzing the financial situation of

companies and its methods in detail.

All the methods mentioned above have their own

advantages and disadvantages. We will discuss these

further in the future.[7]

ACKNOWLEDGMENTS

The author thanks Kayumov E. and

Ataniyazova M., professors and teachers of Tashkent

University of Applied Sciences, for their scientific

and practical help in writing this article.

List of Used Literature

1. Abdukarimov I.T. Methods of Reading

and Analyzing Financial Reports. "Economics and

Law World" Publishing House, 1998.

2. Bakanov M.I., Sheremet A.D. Theory of

Economic Analysis. - Moscow: Finance and

Statistics, 1995.

3. Beganov V.S., Shaulov D.I., Kan U.T.

Features of Accounting in Joint Stock Companies. -

Tashkent: Publishing House "World of Economics

and Law", 1998.

4. Volojin I.O., Ergashboyev V.V.

Financial Analysis. - Tashkent: "Economics and

Law World" Publishing House, 1998.

5. Kovalev V.V. Financial Analysis. -

Moscow: Finance and Statistics, 1996.

6. Pardayev M.K. Methodology of

Financial Analysis. - Samarkand: SamKI, 1997.

7. Pardayev M.K. Traditional Methods

Used in Economic Analysis. - Samarkand: SamKI,

1997.

8. Pardayev M.K. Profitability and Profit

Analysis in a Market Economy. - Samarkand:

SamKI, 1996.

9. Petrov V.V., Kovalsv V.V. How to Read

a Balance Sheet. - Moscow: Finance and Statistics,

1993.

10.

Sheremet

A.D.,

Sayfulin

R.S.

Methodology of Financial Analysis. - Moscow:

INFRA-M, 1996.

11. Financial Analysis of Firm's Activities.

- Moscow: "Krokus - International", 1993.

Basic tools (AV

)

Intangible assets

(NA)

Long-term laying

Material working

capital (MAM)

Debtors (D)

Cash and valuable

papers (PM)

Self-funding (UM)

Long-term

commitments

(CHJUM)involving

outsiders

Short-term

commitments

(CJSC)

Creditors (KP)