ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

296

FEATURES OF TAXATION OF CONSTRUCTION COMPANIES IN FOREIGN

COUNTRIES AND THEIR USE IN OUR COUNTRY.

Abishov Muxammed Sarsenbaevich

PhD., Karakalpak state university.

Mamutova Amina Rahkmetovna

assistant, Karakalpak state university.

https://doi.org/10.5281/zenodo.10645271

Abstract. This article provides ideas and recommendations on the introduction of tax

incentives for construction projects that provide for an increase in future tax revenues at the

expense of construction works aimed at the construction and development of infrastructure in the

regions through the TIF mechanism, which has been effectively used in developed countries for

several years.

Key words: TIF mechanism, value added tax, "rollback" mechanism, tax base, sales tax

and tax credits.

ОСОБЕННОСТИ НАЛОГООБЛОЖЕНИЯ СТРОИТЕЛЬНЫХ КОМПАНИЙ В

ЗАРУБЕЖНЫХ СТРАНАХ И ИХ ИСПОЛЬЗОВАНИЕ В НАШЕЙ СТРАНЕ.

Аннотация. В статье представлены идеи и рекомендации по введению налоговых

льгот для объектов строительства, предусматривающих увеличение будущих налоговых

поступлений за счет строительных работ, направленных на строительство и развитие

инфраструктуры в регионах через механизм ФТИ, который имеет уже несколько лет

эффективно используется в развитых странах.

Ключевые слова: механизм TIF, налог на добавленную стоимость, механизм

«отката», налоговая база, налог с продаж и налоговые кредиты.

In the foreign practice of taxation of construction companies, there is no special tax regime

for those engaged in this activity, like all taxpayers, they pay taxes based on the land, water

resources, property and activities and financial results used. However, it is still possible to

encounter specific tax cases in accordance with the characteristics of the construction work. For

example, in the UK, a refund mechanism can be cited in the calculation of value added tax, which

has been in effect since 2017 in order to conceal taxes in the construction sector and reduce the

risk of misuse. In the UK, businesses with an annual turnover of more than £ 85,000 will be

required to register as construction companies and VAT payers in general. Typically, construction

companies are taxed at standard 20 percent rates. In calculating the value-added tax, the amount

of the difference between VAT (outgoing VAT) levied on the customer for the construction work

performed and the VAT paid (input VAT) on the purchased construction materials will be required

to be paid to the budget. In case of import of construction materials, the amount of input VAT is

indicated by indicating the increased amounts of VAT, or in cases where construction materials

purchased from privileged enterprises (less than 85.0 thousand and not registered as VAT payers)

are not specified in the invoice In order to eliminate the cases of submission of reports by reducing

the value-added tax payable to the budget by artificially increasing, from 2017 introduced a

mechanism of "refund" of value-added tax. In such cases, not only the supplier, but also the

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

297

construction companies were held liable, and the VAT, which was not paid to the budget, was

fined and "refunded".

In China, an urban development support tax has been introduced to continuously support

urban development and improve financial provision. This tax was introduced on December 1, 2010

and applies to foreign enterprises established on the basis of foreign capital. In this case, the tax

base is calculated on the basis of value added tax, which must be paid to the budget and is classified

according to the location of enterprises:

Table 1

Urban construction support tax rates in China

№

Taxpayer's address

Tax rate

1.

In the cities

7 %

2.

County level towns, settlements

5%

3.

Other regions

1%

Due to the fact that construction work in the United States (US) is carried out at a very high

rate, the income of construction companies is high, and it is most important to address the problems

in calculating the sales tax when taxing them.

Because in some U.S. states, construction

companies pay sales tax based on the volume of construction work, in other states they do not pay

such tax. In Connecticut, for example, sales tax is levied on construction work for industrial and

other commercial use. Similarly, in some U.S. states, construction companies pay sales tax on

purchased materials, while in some states construction companies pay sales tax on materials

purchased as intermediaries without transferring sales work to the final consumer. In most states,

tax exemptions apply to construction materials that are exempt from sales tax, such as church

construction work, and the same applies to materials purchased and the amount of work done. In

this case, a certificate confirming the release of the construction work will be required.

In the developed countries of the world, the issue of increasing the volume of construction

work as a guarantee of sustainable economic development in the current situation of budget

shortages and instability of the macroeconomic environment, the creation and modernization of

infrastructure that will provide tax revenues in the future. Because the global mortgage crisis in

recent years has increased the risk of directing funds for this type of construction, which in turn

has led to the emergence of a special direction of financing construction work carried out at the

expense of the budget. Today, there are many potential sources of social infrastructure

development, and these resources are used to some extent for infrastructure development, but the

results of their use are not significant enough for economic development. One of the problems in

the practical use of many resources for infrastructure development is the distribution of risks of all

participants in the investment process, the projects are not linked to the economic development of

1

Taxation in the construction industry. Antony Seely. Commons Library Briefing, 9 September 2019. P. 37-39.

http://researchbriefings.files.parliament.uk/documents/SN00814/SN00814.pdf

3

It is known that the United States has introduced a sales tax and there is no value added tax.

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

298

the regions and

can not fully

realize

the

benefits

based

on the principles

of

increasing

additional

tax

revenues

from

economic

growth. As a

result,

the

construction of

infrastructure

does not take

precedence

in

the development

of the regions

and increase tax

revenues. To solve this problem, the developed countries of the world use various mechanisms of

infrastructure development, which provide for the construction of these facilities from the current

taxes and levies, the use of future benefits in the form of benefits, such as investment multiplication

and future budget revenues. This mechanism is known worldwide as the Tax Increment Financing

(TIF), which is also part of the investment mechanism to increase construction work to increase

tax revenues in the future. In recent years, this mechanism has aroused great interest in developing

countries, as well as in developed countries.

Prospective tax revenue growth financing ( TIF) is a model for financing the construction

of infrastructure by increasing future tax revenues from planned improvements in the region. To

implement an infrastructure project financed using TIF, the competent authorities allocate a

specific area ( TIF-area), which, in addition to the infrastructure facilities to be built, also includes

residential, commercial or industrial real estate.

At the beginning of the project, the amount of tax revenues (real estate taxes, land taxes,

taxes on business activities operating in the region) will be calculated in advance and the forecast

will be determined. The implementation of infrastructure in the region is expected to increase the

value of real estate and land in adjacent areas, increase tax revenues without changing tax rates. In

order to reduce the cost of construction work in the TIF-area and reduce the cost of financing the

project, the practice of tax exemption for construction work performed in the area can be applied

in some cases. In order to provide such tax benefits to construction companies, local authorities

must have the authority to provide tax benefits.

5

Strickland, T. (2013) The Financialisation of urban development: Tax increment financing in Newcastle upon-Tyne,

Local Economy, 28(4), 384-398.

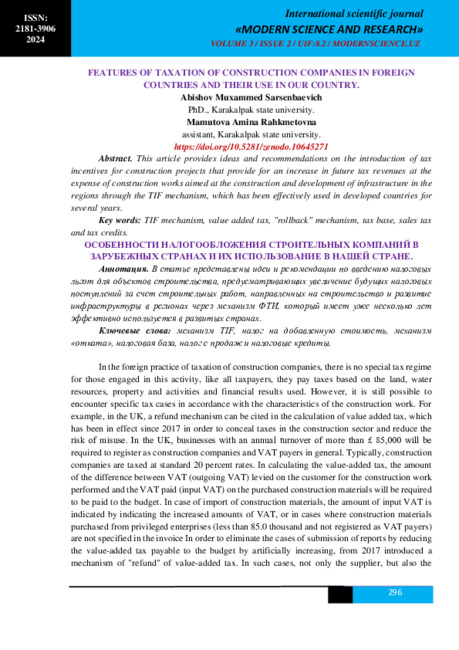

As a result of the TIF project, along with the expansion of the

source of income, there will be other socio-economic benefits: new

jobs will be created, the quality of services provided to the

population will increase, and so on. This in turn serves socio-

economic development.

Of the TIF project

beginning

TAX R

EVE

NU

ES

Of the TIF project

finish

Tax receipts before the project is launched

Increased at the expense of the TIF project

incoming income

Ta

x a

s a

r

esul

t of the

proje

ct

PERIOD OF PROJECT IMPLEMENTATION

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

299

Figure 1. Stages of implementation of the construction project to finance the growth of

future tax revenues.

Subsequent implementation of the project may lead to an increase in revenues from sales

taxes or value added tax, an increase in the number of jobs, but these factors are considered

secondary factors, the main factor is the increase in land and property taxes due to infrastructure

development. increase is considered. The term of the TIF project is predetermined and is usually

20-25 years. When the project is completed, all the high revenues will go back to the budget.

This tool is mostly used by local authorities to finance the construction of certain infrastructure

facilities or complex development projects in certain areas. The reasons for considering the

possibility of using the TIF mechanism for this in the complex development of individual regions

can be divided into global and regional (local) reasons. Global (goal - higher socio-economic

development based on existing and developed infrastructure) reasons:

• Counteract the decline in economic development of the regional structure, including the

decline in tax revenues;

• Stimulation of population flow to the regions;

• Attracting private investment to the city;

• Facilitate the development of the regional structure within the framework of previously

defined comprehensive development plans.

Territorial (goal - to develop infrastructure in a particular area) reasons:

• Reconstruction of the district due to its obsolescence;

• Reconstruction of the district due to a change in the purpose of its use (for example, the

transformation of a residential area into a business center);

• expansion of the district;

• the need to build the district from scratch;

• Improving the environmental aspects of the district (relevant for former industrial areas).

The practice of using the TIF mechanism in the United States.

One of the key features

of the proliferation and application of the TIF mechanism in the United States is that these

processes are not regulated by law at the federal level. Due to the high level of regional and

municipal autonomy, the spread of TIF in the U.S. in the legislative, budgetary, and taxation

processes has historically occurred at the level of states and municipal structures. The concept of

shaping the TIF mechanism was developed in the early 1940s. In 1945, the necessary legislative

framework for the establishment of TIF-districts in California was formed, in 1951 the state tax

legislation was amended, and in 1952 it became the first state to allow the use of the TIF-

mechanism to finance infrastructure projects.

Following California, similar legislation was passed in Rhode Island (1956), Nevada

(1959), Oregon (1960), and in the late 1960s in two other states. By 2003, the TIF regulatory

framework appeared in all 50 states and the District of Columbia (the last being Massachusetts),

6

Compiled by the authors

7

It should be noted that a number of sources point to Tennessee as the first state to allow ISTOM (TIF) legitimacy.

Indeed, in Tennessee, as early as 1945, legislation was enacted that allowed the use of an ISTOM-like mechanism to

finance infrastructure development.

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

300

but currently 48 of them (with the exception of Arizona and California) have project management

through TIF.

The practice of applying the TIF mechanism in the UK.

In England and Wales, the legal framework for the application of the TIF mechanism

was established at the national level: the LocalGovernmentFinanceAct was adopted in 2012 and

entered into force in April 2013, extending to England and Wales, expanding the tax authorities

of local governments. Prior to the enactment of this legislation, local governments did not control

the distribution of local taxes on commercial real estate (BusinessRate or Non-domesticRate):

this tax went to the central government and was then distributed in the form of targeted grants

(RevenueSupportGrant). The new legislation introduces a system of withholding tax revenues to

finance construction work from the value of commercial real estate. The legislation provides for

two mechanisms for withholding tax revenues in favor of local authorities:

• Regular withholding of 50% of all tax revenues from commercial real estate in

accordance with the basic tax base, as well as withholding of up to 50% of tax revenues related

to the increase in taxes on commercial real estate;

• Establishment of special districts where it is possible to deduct 100% from the growth

of tax revenues from the value of commercial real estate.

The first of the above mechanisms cannot be interpreted as a traditional TIF mechanism,

as it is a measure aimed at increasing the level of decentralization of local authorities and

reducing their financial dependence on the central government. However, the introduction of the

principles of TIF mechanisms is a necessary basis for the transfer of a portion of taxes levied on

commercial real estate located in an area controlled by the local government to the control of

local authorities (district or city authorities).

Previously, all tax revenues of this type were controlled by the central government and

distributed to the regions in the form of targeted grants to cover the cost of servicing municipal

structures, with the required expenditures determined by the Community and Local Government

(Departmentfor Communities, Local Government). In this situation, municipal structures were

not encouraged to develop the commercial sector and attract private investors, because regardless

of financial performance, they were financed from the center, and the increase in the tax base did

not affect the municipal budget.

Since April 2013, municipalities in England and Wales have

moved to a mixed financing system, under which 50 percent of commercial real estate tax

revenues are still controlled and distributed by the central government, while the other half

remains at the disposal of local governments, giving some freedom in allocating budget funds

locally gives.

An important feature of this situation is that the tax base of municipalities will

remain at the level of 2013 ("frozen" level), in the event of an increase in the tax base, this

difference will be transferred to the municipal budget. It is assumed that municipalities will

require a certain amount of funding. In the transition to a mixed system of tax distribution, local

governments will have to cover all costs independently from the tax revenues received, and the

8

Rewiring public services: business rateretention, Local Government Association, December 2013.

9

Local government Finance Act 2012 Guide, Local Government Information Unit.

10

Business Rates Retention. Technical consultation, 2012.

11

A guide to the local government finance settlementin England, 2013.

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

301

local government will provide grants when these funds are lacking. In the transition to such a

system, municipalities do not have the resources to develop cities independently. To provide such

an opportunity, the practice of freezing the tax base is applied, from which the increased tax

revenues can be directed to the implementation of infrastructure projects. In addition, the

legislation allows local governments to borrow for infrastructure development, which is provided

by the potential growth of the debt tax base.

It should be noted that the "fixed" level of the tax

base will be periodically revised. In particular, the tax base is currently set at 7 years, and it is

planned to recalculate it in 2020, after which it will be revised every 10 years. There are also a

number of restrictions at the current stage of the mechanism, which serve to maintain a balance

between the financial flows of municipalities, but this issue is primarily related to the allocation

of budget funds for the daily needs of municipalities. Under the Accelerated Development

Zone

, the central government can grant special tax status to any region that needs the necessary

infrastructure changes to support business development. In such a status, the increase in taxes on

commercial real estate will be fully (100 percent) directed to local governments to assist in

infrastructure development. There is no open source information on how to assess the need for

special zones, but the following can be said in this regard:

• The right to organize territories is vested in the central authorities, in particular, this

issue is within the competence of the Secretary of State for Communities and Local Self-

Government (Secretary of State for Communities and Local Government);

• local authorities have the right to apply for the establishment of accelerated development

zones;

• municipal structures can submit joint applications for the establishment of special zones

and develop projects within the general budget;

• the validity period of accelerated development zones is limited to 25 years;

• There may be a limited number of areas of rapid development at the same time, the total

amount of funding for which may not exceed a certain amount.

At the time of the audit, the maximum limited number of regions was not set by law, the

total funding was limited to £ 150m in 2013, the maximum allowable amount of funding is set

by the central government budget.

Also in 2010, the regulatory framework of TIF was adopted

in Scotland. As part of its inspection, the authorities decided to launch 6 pilot TIF projects.

Territorial authorities do not currently have the right to organize TIF-territories independently,

they must submit projects to central authorities for consideration. In 2014, 3 projects were

approved.

In Canada, the use of the TIF mechanism has only recently begun, as in the United States,

at the regional level: to date, TIF legislation has been enacted in only three provinces, the first

of which was Ontario (2001), where municipal authorities was granted the right to receive.

Relevant legislation was passed by the Manitoba Provincial Government in 2002, but the

first TIF projects in the province were only launched in 2009. TIF-legislation was also adopted

12

The Local Retention of Business Rates Scheme, Helen Burkhalter, Principal Advisor, APSE, 2013.

13

InvestmentandDevelopmentPortfolioReport, NewcastleCityCouncil, 2014.

14

Local government Finance Act 2012 Guide, Local Government Information Unit.

15

Local Government Finance Act 2012 – Non-domesticrates, Mark Upton, LGIU Associate.

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

302

in the province of Albert in 2006, the same year a pilot project for the introduction of the TIF-

mechanism was implemented by the Toronto authorities (under the legislation of the province of

Ontario). In India, in 2012, the Municipal Corporation of Greater Hyderabad

to use the TIF mechanism to develop the city (the terms of the TIF mechanism were also

developed as part of these plans, as such practice did not exist in India or Telangana). In February

2014, the Department of Municipal Administration and Urban Development issued a document

on the use of the TIF mechanism in 800 urban areas. Thus, the TIF mechanism is less widespread

in the world, which is explained by the financial risks associated with the abstraction of TIF-

based revenues, as well as certain difficulties in adapting the existing regulatory environment to

the implementation of TIF. First, the introduction of the TIF mechanism requires changes in the

budget and tax legislation (British experience), in related areas of urban planning, land law,

administrative and civil law, legislation on tariffs. Second, because the mechanism is designed

to be used at the municipal level, it is necessary to change the regulatory framework at several

levels of government. In addition, the use of the mechanism implies that municipal authorities

have the right to regulate taxes and land relations, or are granted such rights. This is confirmed

by the fact that TIF has only been introduced in the countries of the Anglo-Saxon legal system,

which is more adapted to the use of this mechanism, as local governments have more

independence. Expert discussions have shown that the implementation of TIF requires not only

high autonomy of local budgets, but also special institutions that realize the potential of

autonomy. For example, in the US, the municipal bond market, which is one of the main financial

instruments in the implementation of TIF projects, is much easier to regulate than the corporate

bond market, which gives municipal authorities a greater advantage in terms of underwriting

costs. In addition, income from municipal bonds is not taxed and their purchase by large financial

institutions is restricted, which increases their attractiveness to individuals, individuals who are

residents of the areas where TIF projects are implemented (de facto). Often, institutions become

more important because the goals set by TIF can be achieved through other instruments. In

Germany, for example, until recently, municipal banks played a major role in financing social

infrastructure (as in France). In Sweden, a private loan agency purchased municipal bonds, thus

providing revenue for infrastructure financing without the use of a complex mechanism such as

TIF. It should be noted that in the United States, too, the role of municipal mechanisms of

infrastructure financing, including the TIF mechanism, is beginning to be recognized as

insufficient. The U.S. Treasury said in a report in September that local resources were in short

supply and that federal programs, including programs to encourage the use of corporate (not

municipal) bonds, were being developed. The TIF mechanism and similar construction financing

and tax incentives for construction companies participating in this project through modern taxes,

which will allow the socio-economic development of the project area, as well as the recovery of

lost taxes in the future.

The following scientific proposals and practical recommendations for the application of

foreign experience in the implementation of infrastructure construction work in the country,

16

In the countries of the Anglo-Saxon legal system, a special form of city administration with the right of a legal entity

managing large urban settlements.

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

303

aimed at taxing the surveyed construction companies and financing the increase in future tax

revenues, are put forward. First of all, it is expedient to apply the refund mechanism in the

calculation of value added tax, introduced in the UK in order to hide the taxes in the construction

industry and reduce the risk of abuse. It is known that according to the tax legislation, “the

inclusion of value-added tax on the invoice in the sale of goods (services) by non-payers of value-

added tax - entails a fine for suppliers in the amount of twenty percent of the amount of value-

added tax. In this case, the supplier must pay the amount of tax specified in the invoice to the

budget. However, there is no financial liability for construction companies to deduct VAT from

invoices from construction materials suppliers

. In our opinion, based on the experience of the

United Kingdom, it is advisable to apply financial penalties both to companies that supply

construction materials, and to construction companies that receive materials through such

invoices. Because it is possible to determine whether a company supplying construction materials

is registered as a VAT payer through the value-added taxpayer registration software introduced

in the country. Secondly, in order to support the development of the construction industry in our

country, to encourage local investors and improve the financing of construction in cities and

districts, it is necessary to introduce special mandatory payments by local authorities to

construction companies based on foreign experience. In this case, the income from construction

activities can be taken as a tax base, and the rates can be stratified depending on the level of

development of cities and districts. Third, it is expedient to introduce tax incentives for

construction projects that provide for an increase in future tax revenues through construction

work aimed at building and developing infrastructure in the regions through the mechanism of

financing future tax revenues ( TIF), which has been used effectively for several years in

developed countries.

REFERENCES

1.

Taxation in the construction industry. Antony Seely. Commons Library Briefing, 9

September 2019. P. 37-39.

2.

http://researchbriefings.files.parliament.uk/documents/SN00814/SN00814.pdf

3.

4.

5.

Strickland, T. (2013) The Financialisation of urban development: Tax increment financing

in Newcastle upon-Tyne, Local Economy, 28(4), 384-398.

6.

Rewiring public services: business rateretention, Local Government Association,

December 2013.

7.

Local government Finance Act 2012 Guide, Local Government Information Unit.

8.

BusinessRatesRetention. Technicalconsultation, 2012.

9.

A guideto the local government finance settlementin England, 2013.

17

Article 225 of the Tax Code of the Republic of Uzbekistan. National Database of Legislation, 31.12.2019, No. 02/19

/ SK / 4256; 11.03.2020, 03/20/607/0279. https://lex.uz/docs/4674902

ISSN:

2181-3906

2024

International scientific journal

«MODERN

SCIENCE

АND RESEARCH»

VOLUME 3 / ISSUE 2 / UIF:8.2 / MODERNSCIENCE.UZ

304

10.

The Local Retention of Business Rates Scheme, Helen Burkhalter, Principal Advisor,

APSE, 2013.

11.

Investment and Development Portfolio Report, Newcastle City Council, 2014.

12.

Local government Finance Act 2012 Guide, Local Government Information Unit.

13.

Local Government Finance Act 2012 – Non-domesticrates, Mark Upton, LGIU Associate.

14.

Ўзбекистон Республикаси Солиқ кодексининг 225-моддаси. Қонун ҳужжатлари

маълумотлари миллий базаси, 31.12.2019 й., 02/19/СК/4256-сон; 11.03.2020 й.,

03/20/607/0279-сон.

15.

Mamutova A., Ablezova B. THE ROLE OF AGRICULTURAL PRODUCTION IN THE

ECONOMY //Modern Science and Research. – 2024. – Т. 3. – №. 1. – С. 270-273.

16.

Mamutova A., Ibragimov A. IMPROVING THE ANALYSIS OF FINANCIAL RESULTS

IN BANKING INSTITUTIONS //Modern Science and Research. – 2023. – Т. 2. – №. 10.

– С. 561-567.

17.

Sarsenbaevich A. M., Omirbayevna T. G., Ilham N. Ways to Increase the Influence of

Taxes in The Development of Financial and Economic Activities of Construction

Enterprises //International Journal on Economics, Finance and Sustainable Development.

– 2021. – Т. 3. – №. 5. – С. 85-90.

18.

Esbosynovna T. G., Sarsenbaevich A. M. PROBLEMS WITH FINANCING EXPORT OF

AGRICULTURAL PRODUCTS //EPRA International Journal of Economic and Business

Review (JEBR). – 2022. – Т. 10. – №. 6. – С. 5-8.

19.

Esbosynovna T. G., Sarsenbaevich A. M., Saparbaevich K. A. Current Situation of

Agricultural Product Export Financing and its Analysis //Periodica Journal of Modern

Philosophy, Social Sciences and Humanities. – 2022. – Т. 9. – С. 4-11.